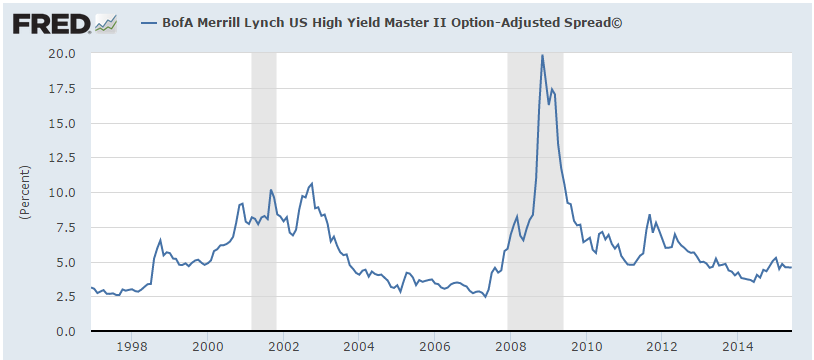

As per Bloomberg report below, a total of $85 Billion in junk loans have been raised this year to finance acquisitions, topping 2007’s record pace. This should not come as a surprise to the readers of this blog. While most market pundits will see this as a positive economic development, it is anything but that. It is a symptom of the financial system that has gone awol.

A system where the Central Bank and the US Government encourage speculation and massive asset bubble creation. A system where the capital is miss allocated and only the rich benefit. Unfortunately, this sort of a financial stupidity can only lead to one thing. An eventual collapse of our financial system and a severe US Recession. As such, you should not view this “Junk Bond” surge as anything other than a proverbial market TOP Bell.

This is further confirmed by our mathematical and timing work showing a severe bear market between 2014-2017. If you would be interested in learning when such a bear market will start (to the day) and it’s internal composition, please Click Here.

Did you enjoy this article? If so, please share our blog with your friends as we try to get traction. Gratitude!!!

Click here to subscribe to my mailing list

Junk Bonds Surge Past 2007 Top. What It Says About The Stock Market Is Beyond Disturbing Google

Bloomberg Writes: Junk Buyout Loans Eclipse ’07 Record in Dealmaking Frenzy

The U.S. junk-loan market has never fueled so much dealmaking.

A total of $85 billion of loans have been raised this year to finance acquisitions, topping 2007’s record pace, data compiled by Bloomberg show. Issuance is set to accelerate as Avago Technologies Ltd. locks in the year’s second-biggest loan for its takeover of chipmaker LSI Corp. as soon as today and Men’s Wearhouse Inc. (MW) borrows $1.1 billion to fund its deal for Jos. A. Bank Clothiers Inc.

Leveraged loans are booming as the value of takeovers in the U.S. reaches levels last seen in 2008. While regulators have warned excesses may be emerging in riskier parts of the market as the Federal Reserve’s zero-interest rate policy extends into a sixth year, the loan surge underscores renewed confidence in the ability of the least-creditworthy companies to expand as the world’s largest economy strengthens.

“There’s a lot of money waiting to be put to work,” Judith Fishlow Minter, co-head of U.S. loan capital markets at Royal Bank of Canada, said in a telephone interview from New York. “The market is exceptionally strong.”

Acquisition Debt

Acquisition financing accounted for 29 percent of the $20.5 billion in leveraged-loan issuance this month, rising from 20 percent of overall borrowings in March, according to a JPMorgan Chase & Co. report dated April 11.

The bank is arranging the loan for Houston-based Men’s Wearhouse, which has a B+ rating atStandard & Poor’s, or four levels below investment-grade. The retailer’s Ba3 junk rating from Moody’s Investors Service is one step higher.

Leveraged loans are rated below Baa3 by Moody’s and lower than BBB- at S&P.

“It’s great from a shorter-term perspective to see more supply,” Jamie Farnham, who manages about $7 billion of high-yield bonds and leveraged loans for Los Angeles-based TCW Group Inc., said in a phone interview.

“From a longer-term perspective it’s indicating that you’re in a later part of the cycle,” Farnham said. “This is the time where you shift up in credit quality.”

Private-equity firms are using more debt to finance buyouts.

Rising Leverage

First-lien borrowings at speculative-grade companies equaled 4.2 times their earnings before interest, taxes, depreciation and amortization in the first quarter, the highest since the 4.6 ratio in the last three months of 2007, according to S&P Capital IQ Leveraged Commentary & Data.

A total $760 billion in mergers and acquisitions of U.S. companies were announced in the year ended March 1, according to data compiled by Bloomberg. That’s the most for a 12-month period since April 2008.

“Markets are extremely accommodating for M&A financing,” John McAuley, co-head of U.S. Leveraged Finance at Citigroup Inc., said in a phone interview. “We expect that conditions will remain favorable for some time.”

The $4.6 billion loan being raised by Avago is the biggest since the one obtained by Community Health Systems Inc., a U.S. hospital chain, in January to help fund its $7.6 billion purchase of Health Management Associates Inc., Bloomberg show data show.

The takeover was the largest of a hospital company since 2006, when HCA Holdings Inc. (HCA) was acquired by private-equity firms including KKR & Co. for about $33 billion including debt.

“We’re not in an environment that some could argue we were in pre-crisis,” said McAuley. “Today’s market is still exercising discipline.”

Fund Inflows

The Fed has kept its benchmark rate close to zero since December 2008 to help support an economic recovery after the collapse of Lehman Brothers Holdings Inc. deepened the worst recession since the Great Depression.

After inundating the U.S. economy with more than $3 trillion, the Fed began reducing stimulus by scaling back its monthly bond purchases this year.

Individuals have made deposits into funds that buy junk loans for 95 straight weeks, including a record $63 billion in 2013, according to JPMorgan. The funds this year have attracted $7.8 billion, with last week’s inflow of $48 million being the smallest since July 2012.

‘Hot’ Demand

The loan for Men’s Wearhouse is covenant-light, meaning it lacks financial maintenance requirements that, when violated, can give lenders an opportunity to negotiate with the borrower. About two-thirds of loans this year are without such protections, rising from about half in 2013, according to JPMorgan.

Covenant-light lending is on the rise as the global default rate for speculative-grade corporate debt is projected to decline to 2.2 percent at the end of this year, from 2.3 percent at the end of March, according to an April 7 report from Moody’s. The forecast is below the historic average of 4.7 percent, based on data going back to 1983.

“There’s enough demand for virtually any deal,” John Fraser, a managing partner at 3i Group Plc’s U.S. debt business, said in an interview at the firm’s New York office.

The rise in acquisition loans gives lenders more opportunity to be selective in a “hot” market, according to Fraser, who oversees $3.8 billion of U.S. credit assets for the London-based private-equity firm.

Careful Investing

The Fed, the Federal Deposit Insurance Corp. and the Office of the Comptroller of the Currency updated guidance on lending to speculative-grade borrowers about year a ago, citing “deteriorated” standards and the willingness of investors to accept looser terms.

“You just have to be very careful,” Beth Maclean, a bank loan manager at Pacific Investment Management Co., said in a Bloomberg radio interview on April 11. “There are more aggressive deals being done.”

Collateralized loan obligations, the biggest buyers of junk loans that fueled the 2005-2007 buyout boom, will raise as much as $90 billion in 2014, the most in seven years, based on a forecast fromWells Fargo & Co. this month.

Deals done before the financial crisis were “incredibly large,” with private-equity firms grouping together to back a single buyout, said RBC’s Fishlow Minter.

The strongest single quarter on record for merger loans was when $118 billion were raised in the last three months of 2007, Bloomberg data show. That was the same time when Energy Future Holdings Corp. got more than $20 billion of loans backing its $48 billion buyout by KKR, TPG Capital and Goldman Sachs Capital Partners, Bloomberg data show.

The Texas utility, formerly known as TXU Corp., is negotiating a plan with creditors that would reduce the time it takes to reorganize under bankruptcy protection.

Lenders are still looking for more opportunities to invest in M&A financings and LBOs, according to Citigroup’s McAuley.

“They are overwhelmed with refinancing opportunities, and underwhelmed with strategic financing opportunities” he said.