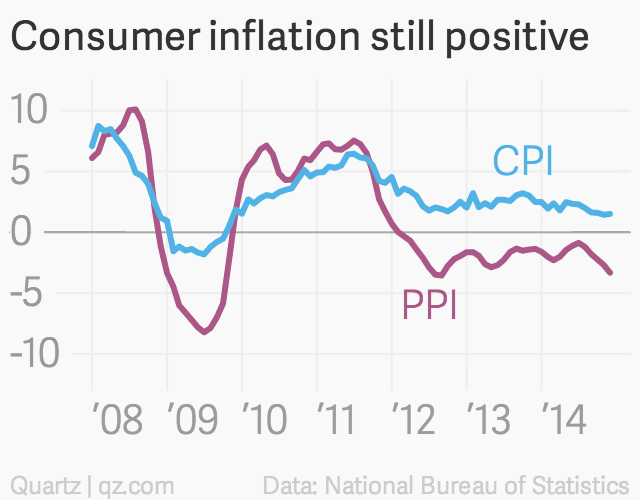

While the Central Bankers in the US are doing everything in their power to avoid deflation, their Brazilian counterparts can’t wrap their heads around Brazil’s accelerating inflation. In fact, the Brazilian Central Bank is widely expected to raise its benchmark Selic rate to a whopping 11% on Wednesday to try and stop accelerating 6.1% inflation. An excellent and a must read article from the WSJ in regards to Brazil if you follow their economy/markets. While my mathematical and timing work shows that deflation and inflation is cyclical in nature (as opposed to fundamental), the WSJ article below brings out a number of important points.

Did you enjoy this article? If so, please share our blog with your friends as we try to get traction. Gratitude!!!

Did you enjoy this article? If so, please share our blog with your friends as we try to get traction. Gratitude!!!

Click here to subscribe to my mailing list

Google

WSJ Reports: With Rates Poised to Hit 11%, Brazil Offers Lessons for the World

The eyes of the world should be focused on Brazil right now — and not just because it will host the World Cup in two months’ time.

It’s also because Brazil’s struggle with rising prices is a reminder that even in this era of global disinflation, flawed policies can years later saddle countries with an intractable inflation problem.

The Brazilian Central Bank is widely expected to raise its benchmark Selic rate to a whopping 11% on Wednesday. It must do so because inflation won’t let up.

Contrast that with the European Central Bank, which Thursday will weigh whether to cut the rate its sets on banks’ deposits into negative territory, all because of data like Wednesday’s euro-zone producer price index, which was down 1.7% on the year.

Brazil is an odd man out in a world where the biggest economies are more worried about deflation than inflation. Despite having jacked up the Selic from 7.5% in the first half of 2013, the central bank last month had to increase its full-year 2014 inflation forecast to 6.1% from 5.6%. That’s well above the midpoint of its target range of 2.5% to 6.5%.

Brazilian society is paying the price for this. The economy has barely grown over the past two years.

It all seems unfair. In most countries with runaway inflation–like Argentina or Venezuela–the blame lies with a central bank that’s manipulated by growth-obsessed governments to keep real, inflation-adjusted interest rates negative. But Brazil’s central bank has for the most part been vigilant. Its rates are even higher than crisis-wracked Turkey’s, where the central bank hiked a key rate to 10% from 4.5% in January to stem outflows from its currency, the lira — both in absolute terms and in real terms.

The roots of Brazil’s problem are mostly structural. Brazilian wages and other contracts are often indexed to inflation–legacy of the hyperinflation of the 1980s and 1990s. That indexing creates a vicious cycle of tit-for-tat price increases to keep ahead of rising costs. There has been discussion for years about how to reduce indexation in the economy, but it’s hard to do so because no one wants to be the first to give up gains.

There’s also insufficient flexibility in the labor market. Despite sub-2% GDP growth for the past three years, unemployment was last cited at 5.1% in February and got as low as 4.3% in December. U.S. and European policymakers would kill for such unemployment numbers. The problem is they partly reflect rigidities. It is difficult to fire workers, which in turn leads to wage inflation.

Add into the mix some rampant government spending attached to poorly budgeted public-works projects — for the World Cup, the 2016 Olympics and port upgrades to enhance the exporting infrastructure — and you have a recipe for inflation.

This is far from Brazil’s hyperinflationary past, when the central bank printed money to finance profligate governments. But even in an era of seemingly responsible monetary policy, the central bank is in a bind.

Self-fulfilling expectations are now entrenched among the population, which believes that inflation — and its corollary, high interest rates — will continue. Business models are built around returns to be derived from those higher rates. There’s also a dependence on funds from abroad as speculators borrow at near-zero rates in dollars, euros or yen andplow that money into far higher-yielding Brazilian reals. This inflow keeps important price-setting sectors of the economy, such as real estate and rents, in a frothy state. It has also begun to bolster what had been a stubbornly weak real, now up 8% versus the dollar from early February — and that’s not good news for the country’s commodity exporters, which have struggled because of a slowdown in China, their biggest market.

Four years ago, the government moved to curtail these dangerous “hot money” inflows by raising taxes on foreign-exchange rates. But it backfired, starving Brazil of foreign capital right when a global slowdown coincided with an exodus from emerging markets as the U.S. Federal Reserve started talking about easing back on monetary stimulus. The policy also gave the central bank an excuse to lower rates, which meant that inflation crept back into the economy.

For those sins — modest as they are — Brazil is now paying the price. The solution does not lie with the Brazilian central bank, but with a government that needs to modernize its labor laws, rein in fiscal excess and dismantle indexation.

How well it achieves that could provide a valuable lesson for others. Once the stimulus policies employed in the advanced countries finally generate the inflation they seek, they will need to ensure that regulations and other structural components of their economies don’t create inefficiencies that breed Brazil-like problems down the road.