Even though Facebook (FB) reported very impressive results for Q1 ($2.5 Billion in revenue and 72% growth y-o-y), the only place it’s stock price is heading is south….way south. While we can talk about the fundamentals, growth projections, user engagement, mobile Vs. PC, acquisition, new revenue streams, etc…… none of such things are relevant to what will happen to Facebook’s stock price over the next 2 years. Here is why……

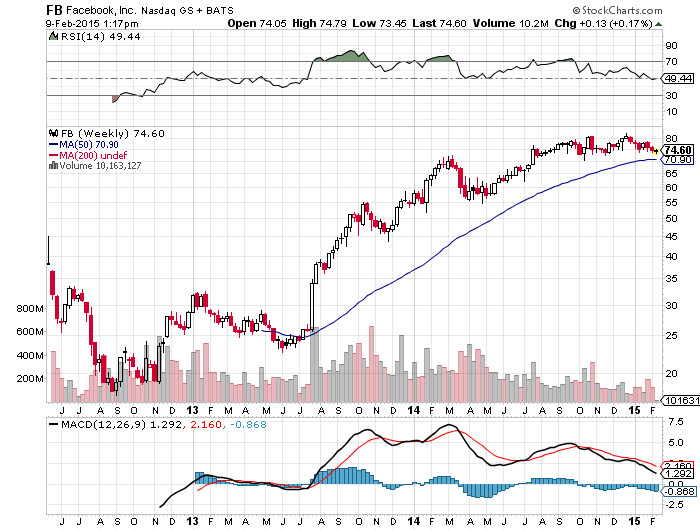

- Highly Speculative & Overpriced: Facebook is selling at about 20 X revenue. I don’t care what the growth or it’s future is, this valuation is extreme. Just as a reference point, two other highly overpriced and speculative companies, Apple (AAPL) and Tesla (TSLA) are selling at 2.6X and 12X revenue. Putting Facebook in a league of it own.

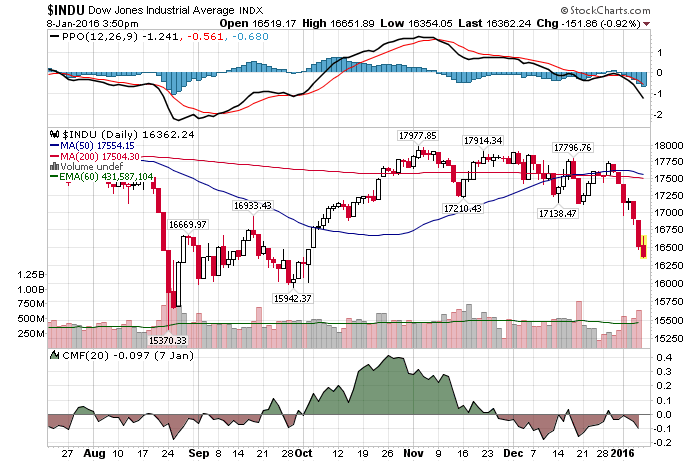

- We Are On A Verge Of A Massive Bear Market: Based on our mathematical and timing work the bear market of 2014-2017 is about to start. When it starts it will very quickly retrace most of the gains accrued over the last few years. High flyers like Facebook will suffer the most. If you would be interested in learning exactly when the bear market will start (to the day) and its subsequent internal composition, please CLICK HERE

In conclusion, based on a simple premise above we believe that Facebook (FB) will see the $20-25 range over the next two years. Basically, at today’s valuation levels, their growth story becomes inconsequential. As you can imagine, right now would be a good time to sell or better yet, go short.

Did you enjoy this article? If so, please share our blog with your friends as we try to get traction. Gratitude!!!

Click here to subscribe to my mailing list

Shocking Secret Revealed: Why Facebook’s Earnings Are Irrelevant & Why It’s Stock Price About To Crash Google

By Alexei Oreskovic

SAN FRANCISCO, April 23 (Reuters) – Facebook Inc has a message for Wall Street: Don’t expect new revenue streams anytime soon.

The world’s No. 1 Internet social network delivered its strongest revenue growth in several years during the first quarter, as its mobile ad business gained steam.

But even as Facebook gave investors the good news, buoying its stock by roughly 3 percent in after-hours trading, the company made it clear that other money-making efforts such as video ads and ads within its Instagram photo-sharing app would not bear fruit in the near future.

“That will probably be the most disappointing statement to come out of the call,” said Macquarie Research analyst Ben Schachter. “Many folks were anticipating a next leg of growth.”

Facebook Chief Operating Officer Sheryl Sandberg told analysts on a conference call on Wednesday that Instagram ads, video ads and a nascent mobile ad network were all still in experimental phases and that none of them would make a meaningful contribution to revenue in 2014.

That may dash the hopes of some investors, who had expected Instagram to start generating revenue two years after Facebook acquired it for $1 billion.

“We’re very focused on consumer growth, and we move slowly and deliberately in monetization,” Sandberg said, referring to the limited number of ads on Instagram. “We don’t see the need or the urge to ramp this as quickly as we possibly can.”

Facebook is also going slow with auto-play video ads. Facebook said earlier this year it would allow a small group of advertisers to display 15-second video ads on Facebook, but Sandberg said on Wednesday the company was still gauging users’ response and was in no hurry to open the service up broadly to advertisers.

The comments are likely to cause financial analysts and investors to re-appraise Facebook’s near-term prospects. In notes to investors released prior to Wednesday’s earnings report, Morgan Stanley estimated that video ads could contribute $900 million to Facebook’s top line this year, while Cowen & Co targeted $1 billion in video ad revenue.

Shares of Facebook remained up in after hours trading, even after the company warned that its advertising revenue growth would slow throughout the year, as it faces tougher year-on-year comparisons.

Investors are willing to give Facebook some leeway, given its strong performance building the mobile ad business, said Macquarie’s Schacther.

“They’ve earned the benefit of the doubt, that even if it doesn’t come this quarter, or the next quarter, that it will come,” he said of the company’s additional revenue opportunities.

TURNAROUND

Facebook’s newsfeed ads, which inject paid marketing messages straight into a user’s stream of news and content, have ignited Facebook’s revenue growth and bolstered its stock price during the past year. The ads are ideally suited for the smaller-sized screens of smartphones and other mobile devices.

Facebook said mobile ads contributed 59 percent of its ad revenue in the first quarter, up from 30 percent in the year-ago period. Facebook’s overall revenue grew 72 percent year-on-year to $2.5 billion in the first quarter, above the $2.36 billion expected by analysts polled by Thomson Reuters I/B/E/S.

Facebook’s first-quarter results underscore how far the company has come since its rocky 2012 initial public offering, when concerns about slowing revenue growth cut its stock price in half. At the time, investors questioned Chief Executive Mark Zuckerberg’s commitment to the financial side of the business, spooked by the hoodie-wearing founder’s comments about that Facebook does not build services to make money, but rather that it makes money to build better services.

Many of the key investor concerns about Facebook’s ability to transition its ad business to mobile phones and a perception that consumers were cutting back their time on the social network have been dispelled, said FBN Securities analyst Shebly Seyrafi.

He noted the proportion of Facebook users who access the site daily increased to nearly 63 percent in the first quarter, up from 61.5 percent at the end of 2013.

“If you look at user growth, engagement rates and monetization, the three key levers of value, Facebook delivered on all three,” he said.

While Seyrafi said he believed Instagram has the potential to turn into a near-term money-maker, he said he was not concerned by Facebook’s comments.

“All these things are new shoots of growth for the company,” Seyrafi said. “But I think that they want to deliver first and report it afterwards, rather than guiding beforehand.” (Reporting by Alexei Oreskovic; Editing by Richard Chang)