Let’s make this very simple. Great quarter for LinkedIn. Pretty much as good as it gets. They lowered their forward guidance, hence the stock sell off. Should you buy?

Not if you like your money. No doubt, LinkedIn is a very well run company. Yet, it is way too expensive for my taste. With about $25 Billion market cap, forward revenue of about $2 Billion and slowing growth, LinkedIn is too richly priced. Certainty, the company will continue to grow at a fast clip, but even a stampede of unemployed workers coming to LinkedIn’s platform (due to upcoming recession) in order to spam each other about job opportunities won’t justify the valuation.

Now, valuation metrics aside, stocks tend to deviate (sometimes significantly) over a short period of time. Is it possible for LinkedIn to surge higher? Sure, but even technical picture is somewhat deteriorating. Today’s down gap is likely to be closed over the next few days. Yet, will LinkedIn and its expensive stock price be able to avoid the pull of the upcoming bear market? Given its rich valuation and slowing growth trajectory, I don’t believe so. If anything, I wouldn’t be surprised to see Linkedin stock price to be cut in half over the next 3 years.

——————————————————————————————–

Here is a good analysis

LinkedIn’s (LNKD) Q4 and FYR lived up to expectations, but guidance was not what the market had hoped for. So once again the usual pounding happened in after hours trading, but to my surprise, not enough if you ask me.

Actually, the company’s results were great and I don’t think investors could have asked much more from the company. Anything more would have been unrealistic. But once again, the problem is not the results or even the guidance, it’s what you pay for it. And in LinkedIn’s case, investors are paying way too much.

I am not going to bother running down the numbers. The company’s results are here and the presentation is here. If you have not read them yet, go ahead and do so …

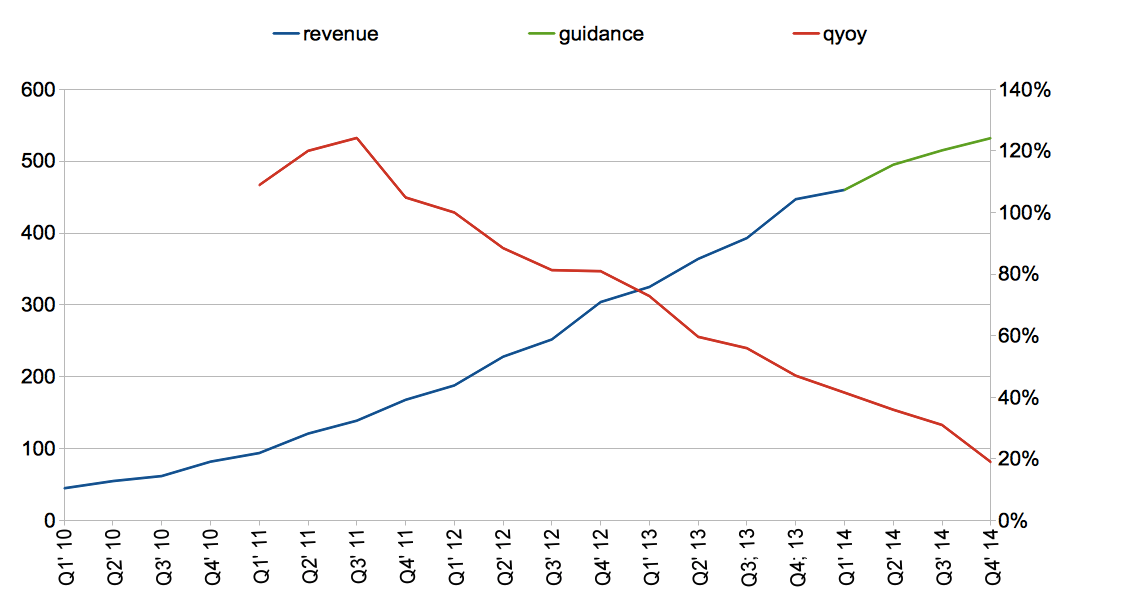

Let me tell you what shocked me from yesterday’s report. Earnings aside and taking only revenue into account, the chart below shows the quarterly revenue of LinkedIn over the past several years.

(click to enlarge)

The blue line is the quarterly revenue of the company up until its recent report. The extension to that, beyond Q4 of 2013 (the green line), are numbers filled in by me based on guidance. In other words, irrespective of the actual results, I started with Q1 of 2014 by plucking in $460 in revenue — which is management’s upper limit guidance — and from there I simply increase randomly revenue every quarter thereafter, so as to come within guidance of $2 billion in revenue for all of 2014 (the green line).

The red line calculates year-over-year quarterly revenue growth. Now up to the most recent quarter, quarterly growth on a year-over-year basis has been coming down since about Q3 of 2011. With the most recent results, it is now down to about 40%. But based on management’s guidance, that will come down to about 20% by the end of 2014.

My question is, is LinkedIn worth $26 billion? Is any company with $2 billion in revenue and with forward guidance of 20% revenue growth worth that much? In my book, LinkedIn is not worth $26 billion even with 50% year-over-year quarterly revenue growth, let alone 20%.

But let me ask investors another question. What will happen if the growth trajectory of the company continues to disappoint further in 2015 and 2016? How much of a multiple will the market put on LinkedIn then, if for example management’s guidance calls for 30% revenue growth in 2015 instead of the almost 50% that the market is expecting? Will the market still pay $26 billion for the company’s stock? My answer is no.

And if you want my opinion, if management disappoints again and the market realizes that the super high growth days are over, then it will mark the stock down beyond what anyone imagines. By how much we will have to wait and see, but even $100 a share is pretty farfetched for LinkedIn’s stock if you ask me.

The market was modeling $2.16 in revenue for 2014 and management gave the market around $2 billion. The market is modeling around $2.9 billion in revenue for 2015 and my guess is that analysts will be bringing that figure down. By how much makes no difference, because even with $3 billion in revenue, there is no reason for LinkedIn’s market cap to be around $26 billion anyway.