(Quick Note: Dear reader….. I can drop a substantial amount of economic and statistical data on you to support the points below. However, if past is any indicator any such economic data would put most readers to sleep within 10 second. Plus, a volume of data/analysis can be published in regards to every single point below. As such, I offer only a quick summary and my conclusion for your reference. Should you require any additional information about the thesis below, please contact me directly. )

Yes, I called it perfectly in 2006-2007 and now I am saying that it is not over.

Before we can understand where we are now and where we are going in the future we must understand where we came from. The Real Estate run up that we have experienced between 1997-2007 has no historical precedent. Real estate data going all the way back to 1790 clearly shows that the US housing market basically appreciated at the rate of inflation. Yes, there were some bubbles and substantial declines, but overall, appreciation at the rate of inflation is an appropriate way to look at the US real estate sector.

A QUICK HISTORY LESSON:

All of that changed in 1997 when Bill Clinton signed The Taxpayer Relief Act into law, basically allowing $250,000 in tax free capital gains in real estate. While real estate was already appreciating at a good clip at that time, that law added fire to the trend.

Later, fearing significant economic slowdown in 2002-2003 the Bush administration added a huge amount of jet fuel to the Real Estate Bubble by cutting interest rates and making mortgage finance available to everyone (even to the dead people). As people used to say, if you can fog a mirror you can get a mortgage. Of course, all of that led to the largest finance bubble in the history of mankind that “kind of” melted down in 2007-2009. I say “kind of” because most of those excesses are still in the financial system and will have to be worked through in the future.

WHERE ARE WE NOW?

Issue #1: US Home Ownership Rate Is Plunging

On historical basis, home ownership rate in the US is in free fall. Take a look at the chart. I think it speaks for itself.

Issue #2: Real Estate Affordability Is Plunging

Take a look at the chart as it speaks for itself. The affordability index is in free fall as well. Most likely due to higher interest rates and rising prices.

Issue #3: Interest Rates Are Going Up

The trend has shifted up and the 10-year rate is up 100% over the last 12 months. I gave detailed interest rate analysis here. Please take a look here.

Issue #4: US Economy & The Stock Market Is About To Turn Down (Big Time)

Please read “The Long Awaited US Stock Market Decline Is Likely Here” as to why.

Issue #5: Who Is Buying All Of These Properties For Cash Today?

Chinese buyers, hedge funds, banks themselves, investors, speculators, etc….. Who cares!!! Remember all those Japanese investors buying everything they could in California and Hawaii in the late 1980’s. I wonder how that turned out for them.

On a more serious note, notice that I didn’t say Average American Family. That is the only category that we should track if we want to accurately predict the future trend in the US Real Estate market. Every other category is irrelevant over the long run. And guess what? They are not buying. See the charts above.

Issue #6: Bear Market In Real Estate (sucks people back in)

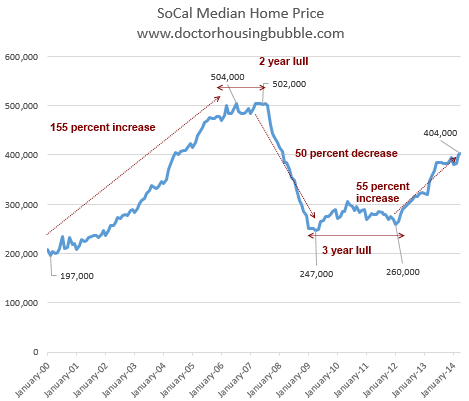

As I have said here before (US Real Estate At A Turning Point), this is how the bear market works. This is the stage #2 bounce, before the big decline (stage #3). The bear market tends to suck people back in, offer them perceived safety and a high return before slamming the door, ripping their head off, drinking their blood and taking all of their money. The US Real Estate market is topping in Stage #2 run up here. That is why you are seeing so many divergences. The market should turn down soon. Beware.

FUTURE OF REAL ESTATE:

Real estate is not made of Gold. There is a tremendous amount of land available in California, Florida and all over the US. There is no housing shortage. As such, expect real estate to decline significantly in order to revert back to its natural inflation adjusted mean. It might take a few years, it might be different for various cities, but one way or another the market will get there.

HOW FAR DOWN?

Let’s do very simple math for the San Diego market. It doesn’t have to be exact for our purposes.

Setup:

- San Diego Median Family Income: $61,500

- As Per Various Financial Guidelines Families Shouldn’t Spend More Than 30% Of Their Income On Housing. That means a $1,500/monthly payment.

- Median Home Price in San Diego: $500,000 (pushing that level again as per Trulia.com)

- Interest Rates: 30 Year Mortgage 4.72% (Rates as of 9/4/2013)

With such fundamental input variables median house value should be $290,000 -OR – A 42% DECLINE ($1,500x360month@4.72%)

What if interest rates go to 7% over the next 5 years, which can easily happen?

The fundamental value of the median house drops further to $225,000 -OR- A 55% DECLINE

Also, don’t forget that markets oftentimes overshoot to the bottom, just as they set blow off tops. In such a case I wouldn’t be surprised to see a median price of $150,000- 200K -OR- A 70%-60% DECLINE

You say impossible….. I say study financial markets. Nothing is impossible.

Now, I understand and agree that there are various market forces at play that make the picture a lot more complicated. Interest rates, timing, mortgage finance, cash buyers, the FED, foreign buyers, speculation, location, supply/demand, etc…. However, fundamentals will always prevail over time. Everything else is just temporary bullshit.

ADVICE:

Your house is not an investment. Don’t be confused. It is the place you live and raise your family. If you are happy with your house, have a fixed interest rate, can afford your monthly payments and don’t care if your house depreciates in value, I would stay put.

If you find yourself in a contrary situation……..I would consider various options.

Did you enjoy this article? If so, please share our blog with your friends as we try to get traction. Gratitude!!!